Credit bureau reporting of home owner associations’ (HOA) assessment is a powerful tool to manage association assessment delinquencies, maintain on-time payments, protect property value and reward on-time paying residents with a boost in their credit score.

This blog covers the key questions on how credit reporting to the bureaus work for home owners associations, and its benefits for HOAs and community management companies. This also provides useful information on how to get started.

What is Assessment Credit Bureau Reporting?

Credit reporting is the collection and distribution of credit information by bureaus such as TransUnion, Equifax and Experian that have gained permission to access consumers’credit reports. Credit bureaus provide this information to creditors like banks, collection agencies, mortgage lenders, and insurance companies, who use it in making financial decisions involving consumers’ creditworthiness and solvency.

Can HOAs report assessments to a credit bureau?

Yes, similar to how it is for credit card or mortgage payments and debts,The Fair Credit Reporting Act allows for the reporting of community association payments and delinquencies to a credit bureau, on behalf of an HOA or condo board. Read more about this in this Memorandum from Oscar Marquis here.

Which credit bureaus report on HOA assessments?

The three credit bureaus that accept Assessment Payment Credit Reporting are Equifax, Experian and TransUnion. Currently, only Equifax and TransUnion accept on-time, late or skipped payments. This mechanism provides an effective balance of positive reinforcement and negative payment habit correction. Find a credit reporting agency that reports all on-time, late or skipped payments to these for a more effective payment incentive and collection program.

What information can an HOA submit to the credit bureau?

On-time, skipped, or late payments can be reported to the credit bureaus. If a homeowner pays assessments on time, this will be reported to the credit bureaus. In return, they will get a boost in their credit score. If an owner is late or has defaulted on assessments, the HOA can report this to the credit bureaus too and it will affect their credit score.

How will the association and property management company benefit from credit reporting?

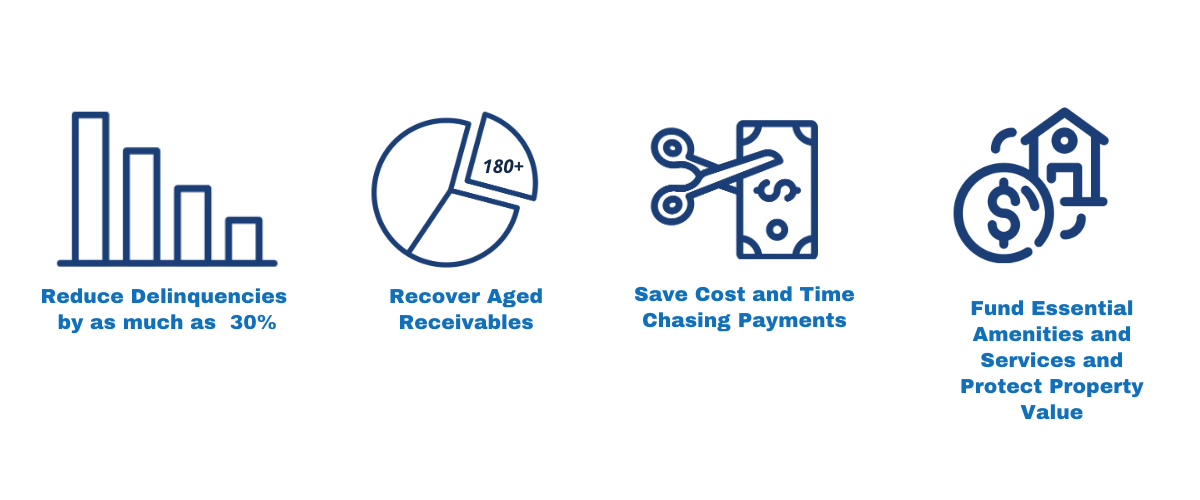

The impact to the credit score, gives an extra motivation for residents to pay on time and avoid their assessments from becoming delinquent. In turn, the association can reduce assessment delinquency by as much as 30%, and recover aged receivables.

With a more predictable cash flow, the association can fund essential property amenities and services; thereby protecting the properties’ value. Since there are less late or delinquent payments, the association or the management company has more time and resources to spend their time on value adding property management services instead of chasing payments. All these benefits and being able to reward on-time paying residents with a boost in their credit score has been considered a competitive advantage of our credit reporting clients.

What are the benefits for the homeowner if their assessments are reported?

According to Experian, people with high credit score often carry a diverse portfolio of credit accounts (e.g., car loan, credit card, student loan, mortgage) which can be an indication of how well you manage a wide range of credit products. If a community reports assessments to the credit bureaus, this adds a new tradeline in their residents’ credit report, thereby increasing the probability of getting a higher credit score. Just like in credit cards, if one pays assessments on time, that gets reported – same goes if one pays late.

What are the benefits of a high credit score?

Consumers put importance to expenses that could affect their score because a high score could:

- Get them lower interest rates on credit card purchases, car payments, home loans etc. vs those with lower scores

- Higher chances of getting approved for credit purchases or obtain credit cards

- Lower rates for insurances

- Determine suitability for a job that requires certain level of security

Can the residents see their credit score?

Yes, every consumer can request for a free copy of th eir credit report from each of the three major credit reporting agencies , Equifax, TransUnion and Experian. One may request for a free copy once a year at AnnualCreditReport.com or call toll-free 1-877-322-8228 .

Does my community association board have control over what gets reported or when?

The HOA board of directo rs has absolute control whether your association’s assessments gets reported or not. However, when credit reporting starts, under the Fair Credit Reporting Act, everyone in the association needs to be reported.

How are accounts on payment plans reported?

Our program recognizes payment plans your asso ciation or property management company has in place. Any account designated to be on a payment plan (including accounts under some form of accommodation due to COVID or other similar hardship) are reported as “on-time, paying as agreed”. They are reported with the balance owed, but $0 of that balance is considered past due. This positive reporting encourages the account holder to comply with the payment plan and build their credit while doing so.

What if account information is reported incorrectly?

If a Data Furnisher like your HOA identifies a needed correction, Sperlonga will submit an update to the credit bureaus and correct any error. This will generally be reflected on a credit report within 24 hours. Sperlonga’s consumer relations department handles all disputes as inclusive to the service. Sperlonga’s service agreement indemnifies and holds harmless the management company and the association for any FCRA concerns. Under FCRA regulations, disputes/investigations must be completed within 30 calendar days

The average time for dispute resolution at Sperlonga is 3 business days. We only need one person from the management company, HOA or data furnisher to verify account information.

How do we get started with credit bureau reporting for HOA assessments?

Sperlonga is a pioneer in the Assessment Credit Reporting space and our credit-reporting experts have streamlined this into a 3-step process.

- The HOA or the Property Management Company Engages with Sperlonga. Schedule a Free Consultation with one of our credit reporting experts.

- Sperlonga facilitates accreditation, setup, and support board/resident education

- Sperlonga reports to the credit bureau each month.

Share this Comprehensive Guide on reporting HOA Assessments to the credit bureaus with your board too!